In short--and, as I'm up waaay past my bedtime, short is what you get--the devil is in the details.

The changes are summarized in the blue book for next Tuesday's meeting, available, here (pdf), and more thoroughly in this attachment (pdf, including a lot of annoying sideways pages). The district is offering two briefing sessions at Central Office on Monday prior to Tuesday's Board meeting (at 4:00 and 6:00), where presumably all this will be hashed out.

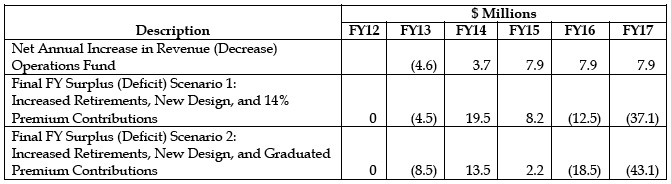

But here's what it looks like: Steep jumps in premiums for either plan, the PPO or the EPO (HMO), and steeper jumps in out-of-pocket costs for both plans. Indeed, the deductibles for the cheaper EPO plan, for example, increase ten times their present amount under the proposal.

The changes in premiums are not unreasonable by themselves. Under the current contract, teachers are paying 1% (single) or 2% (family) of their salary as a premium; here, the premium for most teachers would be either 12% or 14% of the plan cost. The current salary deductions for an average teacher earning $55,000 in base pay add up to about 5% of the plan cost; the change would hit younger teachers harder because the premium shifts from percentage of salary to percentage of the plan cost. And the difference in premium between the EPO and PPO is totally worth it for having broader choice of providers.

But combined with sharp increases in deductibles and out-of-pocket fees, the changes become significantly unreasonable. In the grand scheme, this is because the US health care system is full of crap, providing mediocre quality care at prices the rest of the world just doesn't have to endure, of course, and there's little any one of us can do to change that. But if this goes through, combined with changes to how pensions are calculated, and even assuming no other changes or reductions to the salary schedule after the contract expires in June 2013, teachers in MPS can expect 10%-20% less take-home pay, depending on what their salary is now.

Remarkably, many people will insist that this--like layoffs--is good for the local economy.

(As an aside: I wouldn't be surprised, even given this and the presentation of the facilities master plan report, if the most contentious item on the Board's agenda for Tuesday is the proposed changes to food service.)